Chargeback Management: In-House or Outsourced?

Let’s explore which approach fits your needs.

I’ve been thinking about how to handle chargebacks as I scale my business. Is outsourcing the way to go? Who needs it, and when?

Here, I’ll compare in-house and outsourced chargeback management and answer those questions.

Let’s begin with a clear breakdown of the two.

Key Takeaways

- Managing chargebacks in-house gives control but requires time and resources.

- Outsourcing offers tools and expertise but reduces your control.

- Businesses with high-risk payments often benefit from outsourcing.

- Complex chargeback rules can overwhelm in-house teams.

- AI tools make fraud detection and disputes easier.

- Chargeback tools must work well with your CRM and payment systems.

- Compare costs, growth potential, and industry risks before choosing a method.

If you manage chargebacks yourself, you’ll need effective tools to prevent them. Alerts are one such tool, but they can be tricky to implement. Our platform gives you simple access to all major alerts in one place.

Learn more about how alerts work.

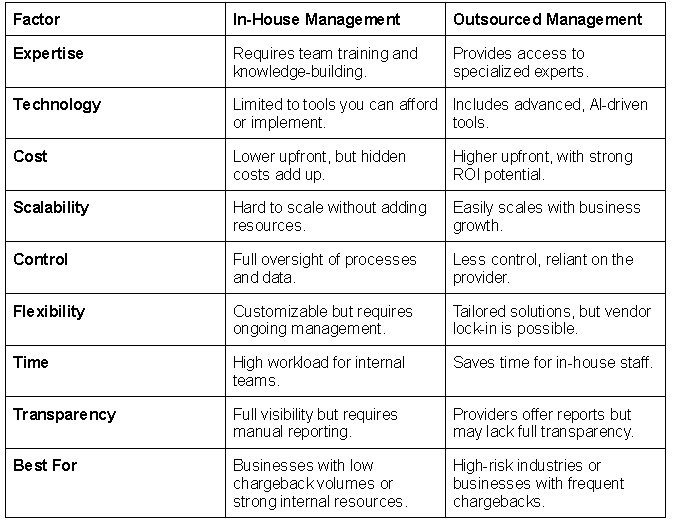

In-House vs. Outsourced Chargeback Management: A Head-to-Head Comparison

In-house management is ideal for small businesses or those with low chargeback volumes. Many tools now make in-house management easier. Reducing the need for outsourcing.

However:

Businesses in high-risk industries or without the expertise to manage chargebacks should consider outsourcing.

We’ll dive deeper into the differences between these approaches shortly.

First, let’s weigh the pros and cons of each.

1. Pros & Cons of In-House Management

Pros

- Full control over chargeback processes and data.

- Customizable processes.

- No third-party access to sensitive financial data.

- Lower upfront costs.

Cons

- Managing disputes takes time and resources.

- High learning curve for teams new to chargeback management.

- Repetitive tasks may lead to staff burnout.

- Limited resources can result in missed disputes.

A study by Accertify found that 46% of merchants struggle with chargeback rules for certain disputes [1]. This complexity makes it harder for in-house teams to manage disputes.

But does outsourcing solve all the problems? Not always.

2. Pros & Cons of Outsourced Management

Pros

- Access to expertise and advanced tools.

- Reduces the burden on internal teams, allowing focus on core tasks.

- Scalable solutions to handle fluctuating chargeback volumes.

Cons

- Vendor lock-in can limit your ability to change providers.

- Some businesses worry outsourcing won’t deliver the best results.

- Loss of direct control over processes.

- Higher upfront costs.

A study revealed that 21% of businesses doubt outsourced providers deliver optimal results. Concerns about transparency and one-size-fits-all strategies often drive this hesitation.

If both options have trade-offs, how do you decide? I’ll help you figure that out soon.

But first, let’s define what “chargeback management” actually means.

What is Chargeback Management?

Chargeback management involves handling and preventing payment reversals. The process includes spotting disputes, investigating claims, and reducing risks. It protects revenue and keeps your chargeback ratio within safe limits.

To address them, you should know how the process works.

Here’s how the process works:

- Identifying chargebacks: Spot disputes fast and gather all relevant facts.

- Taking preventative measures: Use tools and policies to reduce disputes.

- Responding: Submit evidence to fight invalid claims and recover lost funds.

Chargebacks themselves come in many forms. We compare them in a separate piece.

In short, there’s true fraud, friendly fraud, and merchant error:

Chargeback management can involve in-house teams, outsourced partners, or software solutions. For more strategies and tools, check out our guide on chargeback management.

This article focuses on choosing between in-house and outsourced management.

Let’s first explore why chargeback management is so crucial.

Summary: It involves handling and preventing chargebacks.

Why Chargeback Management is Critical

Here are some alarming numbers [2, 3]:

- Financial losses: Merchants worldwide lost more than $130 billion to card-not-present fraud in 2023.

- Operational costs: Could cost an extra $35 for every $100 lost to fraud.

- Monitoring programs: A chargeback rate over 1% can put you in Visa’s Dispute Program. Fines start at $50 per chargeback.

Beyond financial losses, excessive chargebacks can lead to serious problems.

Payment processors may add merchants to the MATCH (Member Alert to Control High-Risk Merchants) list. This database helps banks identify risky merchants. Once listed, it’s hard to secure payment services because banks see these merchants as liabilities.

Sellers on the MATCH list often need high-risk processors. These folks often charge higher fees and demand stricter controls.

Chargeback monitoring programs, like Visa’s Dispute Monitoring Program (VDMP) , also bring heavy fines and extra scrutiny. For example, VFMP fines can start at $10,000 per month and rise to $75,000 if the problem continues.

Do I have your attention?

Let’s explore how in-house chargeback management works.

Summary: Chargebacks cost a lot and can lead to losing merchant accounts.

Managing Chargebacks In-House

In-house chargeback management means your team handles disputes using tools and processes. This includes tracking disputes, gathering evidence, and analyzing trends to reduce future chargebacks.

You’ll need tools like:

- Chargeback alerts: Early warnings to stop chargebacks before they’re finalized.

- Fraud detection software: Tools to identify and block unauthorized transactions.

- Case management systems: Platforms to organize and track disputes.

- Payment processors’ dashboards: Monitor chargeback ratios and payment trends.

We cover these tools in more detail in another guide. There’s no reason to regurgitate the information here.

For now, let’s focus on what you need to succeed with in-house management.

What You Need to Succeed

Managing chargebacks in-house gives you control but requires proper setup. To succeed, you’ll need the right team, tools, and technology.

1. A Skilled Team

Hiring a chargeback analyst can make a big difference. They specialize in fraud patterns, chargeback codes, and gathering evidence.

Your analyst will work with:

- Customer service reps: To resolve issues before they turn into disputes.

- Finance staff: To track chargeback trends.

We can help you determine whether they’re worth hiring in a separate piece we wrote.

If hiring isn’t an option, train your accountant or key staff to handle chargebacks.

2. Essential Tools

Certain tools are must-haves for in-house management:

- Chargeback alerts: Notify you about disputes so you can stop them early.

- Fraud detection software: Flags suspicious transactions before they’re processed.

- Dispute management software: Helps organize evidence and track deadlines.

- Chargeback insurance: Covers losses from fraud that you can’t recover.

Fraud detection software is essential for all merchants. And chargeback alerts are most useful for businesses with high chargeback rates or who sell digital products.

Payment processors like Adyen often include built-in chargeback management tools. Meanwhile, platforms like Shopify offer chargeback protection for eligible merchants.

And insurance coverage will vary by your industry. For instance, Shopify’s protection only applies to physical products from US-based merchants.

To succeed, ensure your tools integrate with your CRM, payment system, and order management tools.

Disconnected systems lead to missed opportunities and poor results.

3. Future-Proof Technology

How do you know if technology is "future-proof"?

Choose tools that are scalable and built to adapt to new fraud trends. AI-powered fraud systems, for example, can evolve with changing fraud tactics.

Make sure your tools also offer regular updates and strong customer support to keep your processes up-to-date.

Next, we’ll explore best practices to maximize your success.

Best Practices for In-House Chargeback Management

To manage chargebacks, follow these best practices:

1. Create a Standard Operating Procedure (SOP):

Have a clear, step-by-step process for handling disputes. Include how to identify disputes, gather evidence, and meet deadlines.

This ensures consistency and improves win rates.

2. Understand Chargeback Reason Codes:

Each chargeback has a reason code that shows the issue, like fraud or customer disputes. Knowing these codes helps your team craft strong responses.

Psst. We have all the codes here.

3. Use Automation and Alerts:

Automated tools reduce errors, help you track cases, and ensure deadlines aren’t missed. This frees your team to focus on strategy and analysis.

4. Analyze Chargeback Patterns:

After resolving a chargeback, look for trends.

Look for common causes like:

- Product categories that attract fraud.

- Fraud triggers, such as high-risk geographies.

- Repeated customer complaints about unclear billing.

Use these insights to fix processes and prevent future disputes.

5. Communicate With Customers:

Many disputes can be avoided through clear, open communication. Train your customer service team to handle refunds and resolve issues quickly to prevent chargebacks.

What kind of challenges might you encounter when going in-house?

Challenges of In-House Management

You may encounter these challenges:

- Limited resources: Managing chargebacks requires time and expertise.

- Solution: Hire a chargeback analyst or use automation tools to save time.

- Knowledge gaps: Teams may not know how to handle chargebacks.

- Solution: Train your team on fraud tactics, chargeback codes, and updates.

- Reactive processes: Teams often focus on responding instead of preventing chargebacks.

- Solution: Analyze past cases to identify problems and improve prevention.

- Scalability issues: Growing transaction volumes can overwhelm small teams.

- Solution: Use automation to handle more disputes without hiring extra staff.

- Risk of errors: Missed deadlines or incomplete evidence lead to case losses.

- Solution: Set up a clear SOP and use tools to track deadlines.

- High costs: Training, tools, and dedicated staff add to expenses.

- Solution: Evaluate costs to see if outsourcing is a better option.

You’ve seen one side. Let’s check out the other.

Outsourcing Chargeback Management

Outsourcing chargeback management means hiring a third-party provider to handle disputes for you. These providers specialize in preventing and resolving chargebacks using advanced tools.

Common services include:

- Fraud prevention: AI tools that detect and block fraudulent transactions.

- Dispute management: Handling cases with precision and meeting all deadlines.

- Data analysis: Identifying chargeback patterns to prevent future disputes.

- Expert advice: Helping you lower your chargeback ratio and stay compliant.

Outsourcing saves time, reduces errors, and often improves win rates. But it’s not for everyone.

Let’s explore why businesses choose this option, what to look for in a provider, and common concerns.

Why Businesses Outsource

Managing chargebacks in-house can take a lot of time and resources. Especially for companies with high transaction volumes or limited expertise. Outsourcing lets businesses focus on their core operations while specialists handle disputes.

Another benefit is access to advanced technology.

Outsourced providers often use AI fraud detection tools and early warning systems to catch fraud trends. Most small businesses can’t match this level of prevention on their own.

These systems provide an edge in preventing chargebacks. Something many businesses cannot achieve with in-house resources alone.

Expertise is another advantage.

Providers have teams that specialize in chargeback codes, representment strategies, and compliance. Their experience often results in higher success rates. They also offer better insights into chargeback causes.

For growing businesses, outsourcing offers scalability. As chargeback volumes increase, third-party providers can easily adapt to handle the workload.

If outsourcing feels like the right option, here’s how to choose a good partner.

What to Look for in an Outsourced Partner

What you’d need varies by industry, but in general, consider these factors:

- Expertise: Look for a proven track record in chargeback prevention and resolution.

- Technology: Choose providers with AI tools and data analytics.

- Integration: Ensure their tools work with your CRM, payment processor, and other systems.

- Transparency: Pick a partner who provides clear reports on performance and fees.

- Scalability: Make sure they can handle your current volume and future growth.

Let’s compare 2 chargeback management solutions, Chargebacks911 (CB911) and Kount.

Kount excels in fraud prevention, CB911 doesn’t. Thus, you’d want the latter only for non-fraud-related disputes. If the chargeback type doesn’t matter, know whether they’ll integrate with whatever software you use.

Before you pick a partner, you should know the following…

Common Concerns About Outsourcing

Businesses often worry about outsourcing.

Here are common concerns and how to address them:

- Loss of control: Companies fear they’ll lose oversight of the chargeback process.

- Solution: Choose a provider with real-time reporting and collaboration tools.

- High costs: Outsourcing may seem expensive for small businesses.

- Solution: Compare costs and consider the ROI from reduced fraud and higher win rates.

- Data security: Sharing sensitive data with a third party raises concerns.

- Solution: Choose providers that comply with PCI DSS and other security standards.

- Lack of customization: Businesses worry providers won’t meet their specific needs.

- Solution: Find partners offering flexible services tailored to your industry.

- Reliability: Concerns about poor service or accountability are common.

- Solution: Check reviews, case studies, and the provider’s track record before signing up.

We’ve covered both sides. However. You may not know which route to go with. I have you covered.

Factors to Help You Decide

Deciding between in-house and outsourcing depends on your business.

Consider these factors:

1. Business Size and Resources:

Smaller businesses often benefit from outsourcing. Larger companies may prefer in-house management to keep control.

2. Chargeback Volume:

High volumes can overwhelm in-house teams. Outsourcing is better for handling heavy workloads. Meanwhile, smaller volumes may work fine in-house.

3. Industry:

High-risk industries like gaming or travel face more fraud. Outsourced providers with industry expertise can help manage these challenges.

4. Access to Technology:

If you don’t have advanced tools like fraud detection or chargeback alerts, outsourcing gives you access to better resources.

5. Budget and ROI:

In-house management might seem cheaper, but costs like training and tools add up. Outsourcing has higher upfront costs but often delivers better results in the long run.

I hope some of what I wrote helped.

FAQs

How Secure Is Outsourcing Chargeback Management?

It depends. Outsourcing is secure if you work with a provider that follows PCI DSS, GDPR, or other data protection rules.

What Chargeback Rate Should I Have?

Keep your chargeback ratio under 0.65% to avoid penalties from card networks.

Wrapping Up

Every business needs chargeback management, but outsourcing may not be the best choice for everyone. Smaller businesses should focus on cost-effective tools, while larger or high-risk companies may benefit from outsourcing.

Our chargeback alerts have helped reduce chargeback rates by up to 91%. They integrate with most major payment processors and provide valuable insights.

Sources

- [1] ROI Analysis: In-House vs. Outsourced. Accertify. 11/29/2021.

- [2] Ecommerce fraud trends and statistics. Mastercard. 1/24/2024.

- [3] Chargeback statistics. Fit Small Business. 2/08/2024.